Travel

4 minutes

GPR 2026 Trend 2: Glocalization is reshaping global commerce

Consumers expect payments to be effortless, wherever they are and wherever they’re going.

Key points:

- Payments are becoming “glocal” – local methods are increasingly expected to work across borders.

- Interoperability is scaling – bilateral links like UPI–PayNow and UPI–PromptPay, plus wider regional Project Nexus, are connecting real-time payment systems across borders.

- Europe is building a payments hub – Wero aims to combine payment systems for broader and easier cross border payments.

- Cross-border solutions from fintechs and payment service providers are scaling – networks like Alipay+ and TenPay Global extend domestic wallets abroad.

Commerce doesn’t stand still, and these days, neither do payments. People are constantly on the move and customers expect to pay with the same ease wherever they are.

Local payments have often evolved to be quick and easy because they were designed for domestic use – built to serve local markets, currencies and meet local regulations. That works for a world where commerce is largely contained within borders, but can create friction when commerce is inherently global, as it is today.

That friction is now being engineered out of the system. We’re calling the move to serve global consumers with a local feel, “glocalization.”

Can domestic systems meet global expectations? They’re starting to.

Cross-border commerce has traditionally been complicated for both travellers and businesses. Unfamiliar or confusing payment methods can result in abandoned transactions and chargebacks. Because of fragmented regulations, systems and preferences, merchants can struggle to localise effectively.

Consumers, though, don’t think of domestic versus international; they think about whether it feels familiar and convenient. The best payment experiences feel like home, even when you are not.

These rising expectations are helping to reshape the payments ecosystem.

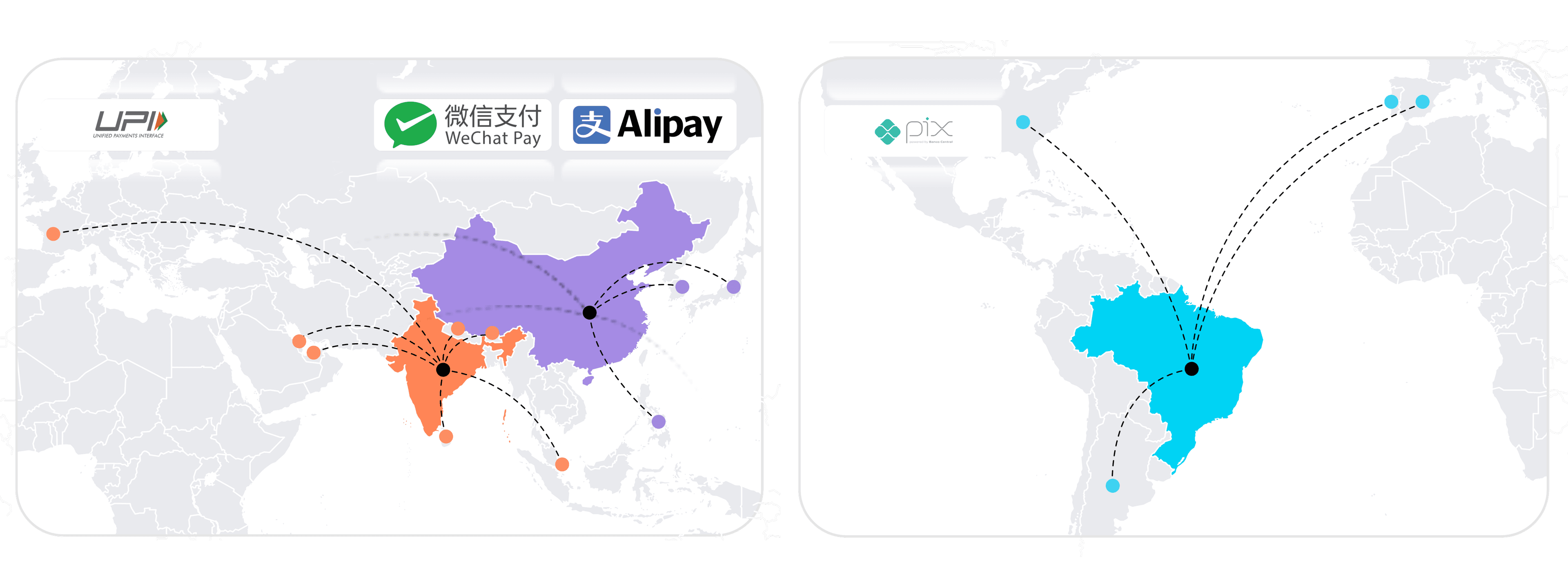

A multipolar payments world is taking shape

Chinese digital wallets like Alipay and WeChat Pay are now accepted by merchants in destinations popular with Chinese consumers. India’s Unified Payments Interface is moving into markets across Asia and the Middle East. Brazil’s Pix is gaining traction beyond its domestic base, connecting consumers and merchants across borders.

The result is a multipolar payment world where multiple dominant systems coexist. This builds on what card schemes have enabled for years, providing similar ease for customers in markets that aren’t card-based.

Interoperability unlocks a world of payments

Interoperability is the key mechanism that makes glocalization possible.

In APAC, bilateral connections between real-time payment systems are already live. India’s UPI links with Singapore’s PayNow and Thailand’s PromptPay, enabling fast cross-border payments. Regional initiatives like Nexus Global Payments (NPG) aim to scale this model, creating shared infrastructure across multiple countries.

In Europe, the approach is more hub-based. The European Payments Initiative’s new A2A payment app, Wero, aims to unify fragmented systems through a shared interoperable layer to enable faster, secure and more effective payments across the region.

Different regions may be taking different routes, but the objective remains to make cross-border payments feel as local – and effortless – as possible.

Domestic wallets are going further than before

Wallet acceptance networks are extending the reach of domestic ecosystems, so people can pay with familiar methods in more places. Solutions like Alipay+ and TenPay Global connect merchants to large consumer bases, bridging domestic payment schemes and international commerce.

Thomas Heldorff, VP of travel, airlines and hospitality at Worldpay, sees glocalization as a competitive lever.

“While global card schemes were originally built with international travel in mind, many of today’s fastest‑growing payment methods were designed for domestic use and local regulations. Cross-border acceptance is now key, and payment method variety is a competitive advantage.”

For consumers, it’s simple: the wallets they trust at home should work when they travel, reducing surprises at checkout and making cross-border spend feel easy.

“Enabling customers to view and pay in their home currency can help increase both spend and purchase confidence,” continues Heldorff. “For example, for airlines, when payments feel familiar, frictionless and trusted, travellers are more likely to complete bookings, upgrade, and engage with add-ons throughout their journey.”

As Marco Chardi, head of research at Worldpay, puts it:

“These days, payment systems should travel with you. The GPR 2026 shows this is starting to happen, with greater interoperability and extended systems flexing with customers on the move. As well as being better experiences for them, this helps merchants expand their audiences, take more payments and ultimately grow their revenue.” Read this year’s Global Payments Report.

Find out more about how Worldpay can serve enterprise customers, including for travel and airlines.

Related insights